Why the refund policy gets more attention than the return policy

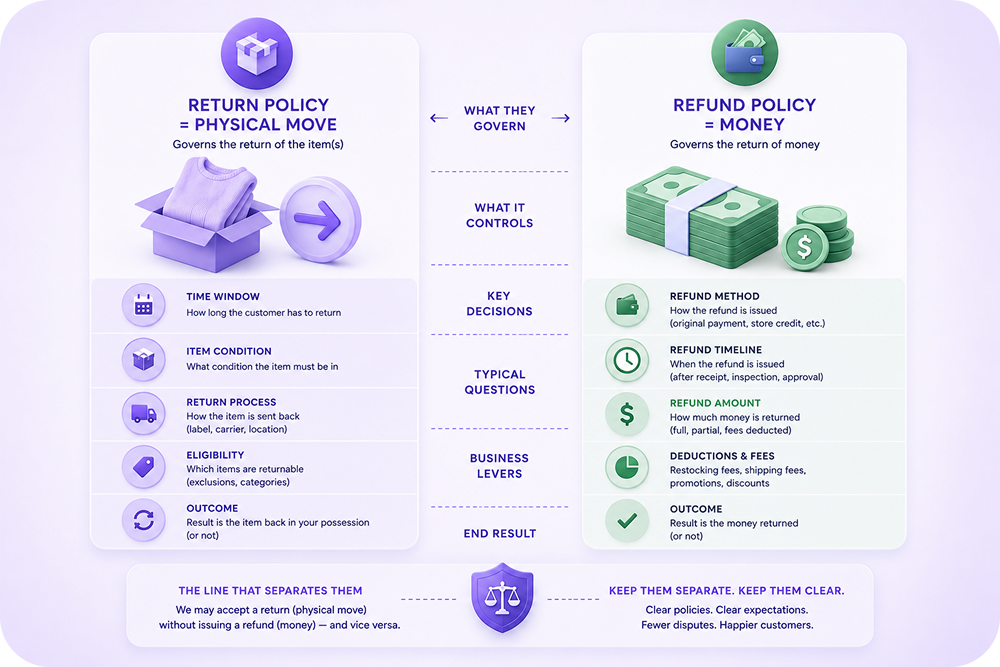

The return policy is about the physical move. The refund policy is about the money. Two different decisions, two different risk profiles, and most ecommerce brands collapse them into one paragraph on a help-centre page. That is where the friction starts.

Refund policy decisions sit at the intersection of finance, legal, customer service, and brand. Every line in the policy affects all four. A policy that protects margin too aggressively kills repeat purchase rate. A policy that refunds liberally cannot survive a fraud wave. The right answer is a layered approach with rules that match the situation, not a single number. For the upstream return policy view, see ecommerce return policy strategies.

What a refund policy actually has to do

Five things, in order of weight.

Set the customer's expectation up front

The number-one driver of refund-related complaints is mismatched expectation, not policy stringency. Customers tolerate a 10-day refund timeline if the page says 10 days. They do not tolerate "fast refunds" turning into 14-day silence. The cleanest version of this principle is in how to notify customers during the returns process.

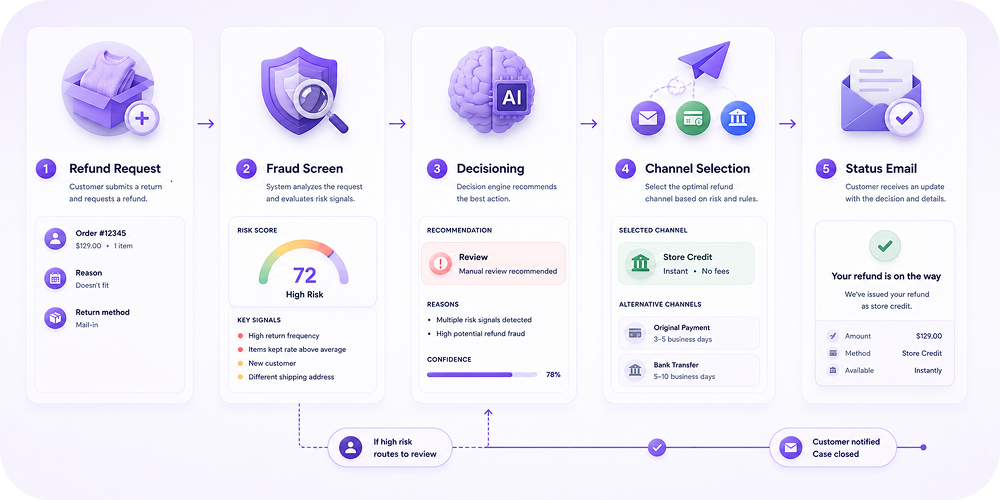

Match the channel to the situation

Refund to original payment, refund to store credit, exchange, repair, refuse. Five channels, each with a different cost and a different customer reaction. The policy should specify which one applies in which case. The existing piece on store credit vs refund walks through the trade-offs.

Define the window

How many days from delivery does the customer have to request a refund. Where the policy splits between defective and non-defective. What happens if the customer opens the package vs not.

Cover the fraud edge cases

Empty box, substitution, wardrobing, friendly fraud. The policy needs language that lets the system pause or refuse a refund without legal exposure. Article 5 of this batch covers the playbook in detail: return fraud prevention.

Spell out the operational steps

What the customer does, what the brand does, in what order, in what timeframe. Without that, the policy is a marketing page, not an operating procedure.

The four levers ranked

Timing

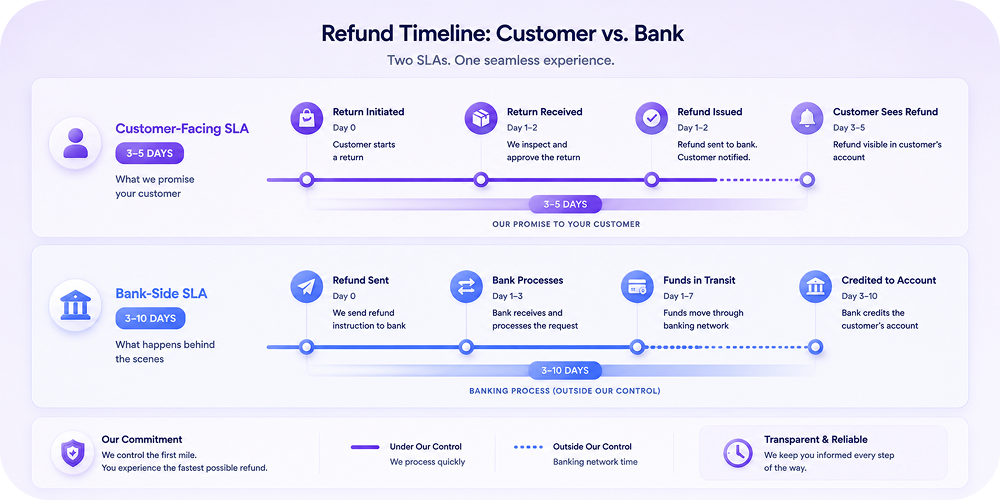

The refund timeline drives more support tickets than any other policy element. Brands that say "refund within 5 business days" and hit that 95% of the time have the lowest contact rate. Brands that promise "instant refunds" and miss the SLA generate complaints whether the absolute time is fast or slow. See the broader pattern in automatic status emails.

Channels

The default refund is back to the original payment method. The lowest-cost refund is store credit or an exchange. The policy should encourage the lower-cost channels without making the customer feel cornered. Returnless refunds in ecommerce covers when to skip the return entirely.

Eligibility

What is refundable, what is not, and on what conditions. Custom orders, perishable goods, intimate items, and digital goods typically have stricter rules. Each exception needs its own line in the policy.

Fraud guardrails

The policy needs language that explicitly allows the brand to pause, refuse, or hold a refund pending inspection in defined circumstances. Vague language opens the door to chargebacks.

The 8 policy elements brands miss most often

1. Who the policy applies to

B2C, B2B, wholesale, dropship. Each has different legal and operational rules. The policy should say which apply to which.

2. Defective vs non-defective rules

Defective items typically have a longer window and a wider eligibility set than non-defective returns. The policy should split them clearly. The optimising the warranty claim process piece covers the defective side.

3. Original payment method default

State explicitly that refunds go back to the original payment method unless agreed otherwise. Removes 90% of the support questions.

4. Refund timing by payment method

Card refunds take 3 to 10 business days depending on issuer. PayPal is faster, store credit is instant. Set the expectation per channel.

5. Partial refunds

When does a partial refund apply? Damaged packaging, missing accessories, late returns. List the rules.

6. Return shipping costs

Who pays. The policy needs a clear answer for each case (free for defective, customer-paid for change of mind, etc.). Compare with the broader free returns pros and cons.

7. Conditional refunds

Pending inspection, pending warranty review, pending supplier approval. The customer should know when their case is in a conditional state and what the SLA is for resolution.

8. The escalation path

What the customer does if they disagree with the decision. A formal escalation path saves chargebacks. See customer service workflows for returns.

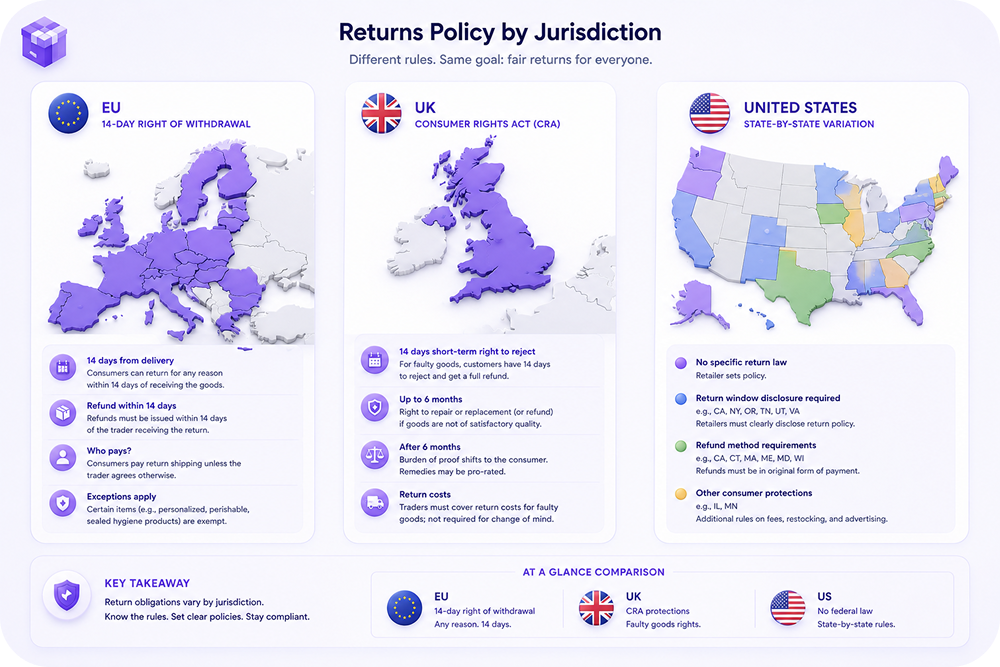

Legal floors in 2026 by jurisdiction

The policy can be more generous than the law, never less.

European Union

The 14-day withdrawal period applies to most ecommerce orders. The customer can return without a reason and the brand has to refund within 14 days of receiving the item or proof of return. Defective products have separate, stricter rules under EU consumer protection. See GPSR for retailers under EU law.

United Kingdom

Consumer Rights Act 2015 governs the floor. 14-day cooling-off period for online sales. Defective goods carry a 30-day short-term right to reject, then a six-year general warranty.

United States

Federal floor is thin (FTC mail-order rules, 30-day timeline if not stated). State law fills in. Brands tend to publish a single national policy that exceeds the federal floor by enough to avoid state-by-state edge cases. The warranty management best practices post covers the broader compliance frame.

Other markets

Australia, Canada, and Japan each have their own consumer protection regimes. Brands serving these markets need a region-specific policy or a clear statement of which version applies.

How AI changes the policy conversation

AI does not change what the policy says. It changes how the policy is enforced. Three operational shifts.

Refund decisioning at the case level

Instead of a rule that says "refund all returned items," the system can score the case and pick the right channel: card, credit, exchange, or hold for inspection. The pattern is the same as in Article 3 on AI for RMA automation and pairs with Claimlane's AI Agent.

Fraud screening before refund

Article 5 of this batch on return fraud prevention covers the screening tactics. The policy needs language that allows the system to act on the screen.

Status communication on every state change

The customer should not have to ask where the refund is. Triggered emails on every state change keep the inbox quiet. Article 1 of this batch on Mailchimp integrations covers the email side.

What the policy looks like operationally

A policy that nobody operates is decoration. Five things have to be true for the policy to land in practice.

Single source of truth

The policy lives in the case system, not in a Google Doc and not pasted into the help centre. When the rule changes, it changes once. The Claimlane workflow engine is built for this pattern.

Versioned and dated

Every policy change should be versioned and dated. Customers who placed orders under v3.2 are entitled to v3.2 rules, not the new v3.3.

Audit trail per case

Every refund decision should record which rule was applied. Three months later, when a chargeback hits, the audit trail is what saves the brand.

Staff trained on the live version

Support teams should be retrained every quarter on the live policy. Memorisation of the previous version is worse than no memorisation.

Reviewed quarterly with finance

Refund policy is half a finance decision. Quarterly reviews with the CFO or finance lead keep the policy aligned with margin reality. See the broader frame in returns and warranty KPIs.

A working policy structure

A clean refund policy fits on one page. The structure that works.

Header

Brand, policy name, effective date, version.

Scope

Markets, customer types (B2C, B2B), product categories covered.

Eligibility

What is refundable, what is not, and on what conditions.

Timing

How long the customer has to request, how long the brand takes to issue, by channel.

Channels

Default refund channel, alternatives, conditions for each.

Process

The exact steps from customer request to money landing. Plain language.

Exceptions and fraud language

Where the brand reserves the right to pause, refuse, or hold pending inspection.

Escalation

How to escalate a disagreement. Email, phone, chat, legal.

Legal disclosures

Jurisdiction-specific statutory rights. Reference to consumer protection authorities.

What to publish vs what to operationalise

The published policy is a customer-facing summary. The operational policy is a longer document that maps every rule to a code, an owner, and an audit trail. They have to match, but they do not have to be the same length.

Customers want clarity in 30 seconds. Operations needs precision across hundreds of cases. The case system bridges the two. See the integrations that make this work in Claimlane integrations and the broader analytics layer in Claimlane analytics.

For brands building the published policy from scratch, return policy generators for ecommerce and return policy templates for ecommerce are useful starting points. Both posts apply to refund policy too, with adjustments.

Common refund policy mistakes

Five patterns repeat across brands.

Promising "instant refunds" when the issuer takes 7 days

Customers blame the brand, not the bank. Be honest about the channel timing.

Hiding the policy behind a login

If the customer cannot read the policy before they buy, the policy is undermined. Publish it.

Refusing refunds via support chat

A support agent should not be the one who refuses. Escalation should be formal, written, and reviewed.

Single policy across categories

Apparel, electronics, and food and beverage have radically different return economics. A single policy oversimplifies.

Not measuring policy outcomes

The refund rate, refund-to-channel mix, and refund SLA hit rate should be on a dashboard. Without it, the policy is theory.

For the operational measurement pattern, see predictive returns analytics for ecommerce and warranty management software.

Frequently asked questions

Conclusion

A refund policy is an operating document, not a marketing page. The brands that get it right separate the money decision from the return decision, write the rules in plain language, and operationalise them inside a single case system. The customer gets clarity, the brand keeps margin, and the support team stops fielding the same five questions every week.

To see how Claimlane runs refund policy inside the same case file as the return, book a demo. Watch the walkthrough on the interactive demo page.

.webp)