.webp)

Ask most brands why their product carries a one-year warranty and the honest answer is that the category does. The number was inherited from a competitor, a supplier sheet, or whatever the last product line used. Almost nobody modeled it.

That is strange, because warranty length is one of the few levers that touches cost, conversion, and retention at the same time. Set it by default and a brand is either leaving money on the table or quietly carrying risk it never priced.

The contrarian position is simple. The optimal warranty period is a finance decision, and it usually is not the number the category copied. Getting there means reading the brand's own claim data, which is exactly what a warranty and return management system exists to surface. Claimlane sees the gap constantly: brands setting terms with no idea what those terms actually cost them.

Why most warranty periods are inherited, not chosen

Warranty length tends to get set once, early, and then never revisited. A product manager picks a term that looks normal, legal signs off that it clears the statutory minimum, and the number sticks for a decade.

The problem is that the inputs change. Failure rates shift as suppliers change, return behaviour changes, and the statutory floor in the EU and other markets already gives consumers more than many brands realise. A warranty that ignores the brand's actual implied warranty obligations is set in a vacuum. Claimlane's role here is unglamorous but decisive: it holds the claim history that should have informed the number in the first place.

What a warranty period actually costs

Every month of coverage is a liability. Finance teams carry it as a warranty reserve, an estimate of future claim cost set aside against products already sold. Stretch the period and the reserve grows. Shorten it and the reserve shrinks, but so does the trust signal.

The useful way to express this is in basis points of revenue and in fully loaded cost per claim. A brand that knows its claim cost by SKU and its failure curve can say what one more year of coverage adds to the reserve, in money, not vibes. That is the level of detail claims and returns analytics is built to produce, and it is the difference between a defensible warranty term and a guess. Reading it next to the brand's other returns and warranty KPIs keeps the decision honest.

The contrarian case for a longer warranty

Here is where the default thinking breaks. A longer warranty is assumed to mean more cost. Often it does. But in the right category it can lower total cost, and the mechanism is not obvious.

Most product failures cluster early, in the first weeks of ownership, then taper. If the failure curve drops off sharply after the early-life period, extending coverage from one year to two or three adds far less claim cost than the headline suggests, because few units fail in those later months. Meanwhile the longer term raises perceived quality, lifts conversion, and reduces the early churn that quietly costs more than the claims do. That connection runs straight into customer lifetime value. For premium and durable goods, the extra coverage can pay for itself, the same logic that drives standalone extended warranty platforms.

Where a longer warranty backfires

The contrarian case has limits, and ignoring them is expensive. A longer warranty backfires when the failure curve does not taper, when the product wears rather than fails, or when the category attracts claims that should be denied because they are outside coverage.

Consumables, wear parts, and products with steady mid-life failure rates all punish extended coverage. So does weak claim verification, since a generous term plus loose proof requirements is an open invitation. The decision is never "longer is better". It is "longer is better for this failure curve, this margin, and this verification standard".

The numbers a brand needs before setting warranty length

Setting the period well takes four inputs, and most brands hold none of them in usable form.

Pull those together and the optimal period stops being a debate and becomes arithmetic. The recovery input matters more than brands expect, because a cost that is recoverable from a supplier should not inflate the warranty reserve. That is the case for tight supplier recovery and faster credit notes.

Warranty length and customer lifetime value

A warranty term is also a marketing asset. It appears on the product page, shapes the buying decision, and signals how much the brand trusts its own product. Treated only as a cost, that value disappears from the model.

The balanced view weighs reserve cost against conversion lift and retention. A term that wins the sale and keeps the customer through a second purchase can outearn the claims it invites, which is the core argument for reading warranty length through a manufacturer warranty lens rather than a pure liability one. Brands that get this right tend to run a clean ecommerce warranty from the start.

Reading claim data to set the period

None of this works on a brand that cannot see its own claims. If warranty data lives in email threads and spreadsheets, the failure curve is invisible and the period stays a guess.

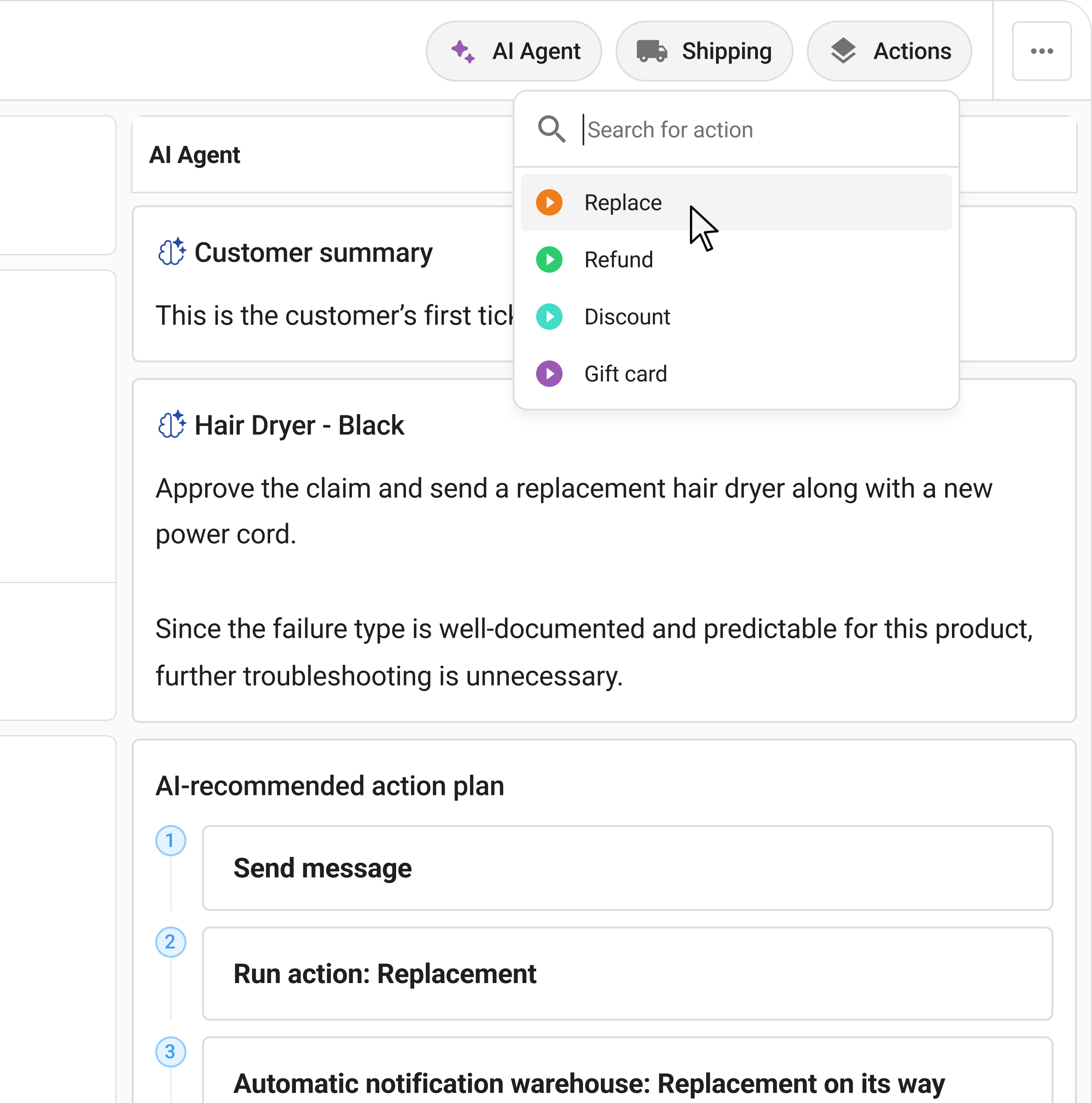

Claimlane captures every claim as structured data: product, serial number, supplier, failure reason, age at failure, and resolution cost. From there the claim workflows and analytics build the failure curve and the cost-by-SKU view a warranty decision needs. Because the data connects to finance and ERP systems like NetSuite and Business Central through Claimlane's integrations, the warranty reserve a brand reports is grounded in real claim history, not a flat percentage someone picked years ago. This is also where it pays to know where Claimlane fits: simple size-and-fit returns belong in a general returns app, but warranty-cost modeling, repairs, and supplier recovery sit with Claimlane.

Registration, proof of purchase, and the real coverage window

One more factor quietly changes the math: when coverage actually starts and whether the brand can prove it. A warranty period means little if the start date and the buyer are unknown.

Product registration pins the coverage window to a real owner and a real date, which both tightens the reserve and improves the claim experience. Pairing the warranty term with product registration software and a clear proof of purchase standard turns a stated period into an enforceable, measurable one.

.webp)