.webp)

Cross-border ecommerce is growing fast, but the duties and taxes that come with it eat into margins just as quickly. For brands shipping internationally or managing cross-border returns, two programs can make a meaningful financial difference: Section 321 de minimis entries and duty drawback.

Section 321 lets shipments valued under a certain threshold enter the US without paying duties or taxes. Duty drawback lets brands recover duties already paid on imported goods that are later exported or returned. Together, they represent one of the most underused cost-saving strategies in ecommerce.

This guide breaks down how both programs work, who qualifies, how to claim them, and how they connect to the returns process.

TL;DR

- Section 321 lets shipments under $800 enter the US duty-free, saving brands 15–25% on import costs for direct-to-consumer orders shipped from overseas.

- Duty drawback refunds up to 99% of duties paid on imported goods that are later exported, returned to suppliers, or destroyed under customs supervision.

- 2025 changes eliminated Section 321 for Chinese-origin goods, but it still applies for shipments from Europe, Canada, and other markets.

- Claimlane's returns data provides the product-level detail needed for drawback filings, especially when returned items are forwarded back to overseas suppliers.

What Is Section 321?

The De Minimis Threshold

Section 321 of the Tariff Act of 1930 allows goods valued at $800 or less to enter the United States duty-free and tax-free. This is called the "de minimis" threshold. It applies per person, per day.

For ecommerce, this means a brand shipping individual orders from an overseas warehouse to US customers can often avoid duties entirely if each package is valued under $800. Instead of paying a 15% to 25% duty on imports, the shipment clears customs with no duty charges.

The $800 threshold was raised from $200 in 2016 under the Trade Facilitation and Trade Enforcement Act. That change dramatically expanded the usefulness of Section 321 for direct-to-consumer ecommerce.

How Section 321 Works in Practice

When a package enters the US through customs, there are several entry types:

- Formal entry (Type 01): Standard import with full duties, taxes, and customs paperwork. Required for commercial shipments above $2,500.

- Informal entry (Type 11): Simplified process for shipments valued $800 to $2,500. Duties apply but paperwork is lighter.

- Section 321 entry (Type 86): For shipments valued at $800 or less. No duties, no taxes, minimal paperwork. Clearance is typically faster.

The Type 86 entry was introduced by CBP (Customs and Border Protection) in 2020 to bring more visibility to Section 321 shipments. Before that, many de minimis packages entered with almost no data, which made it difficult for CBP to screen for prohibited goods.

Who Uses Section 321?

Section 321 is used by:

- DTC brands shipping from overseas factories or fulfillment centers directly to US consumers

- Cross-border marketplaces that aggregate small-value orders

- Brands with bonded warehouses in border zones (particularly US-Mexico and US-Canada)

- Chinese ecommerce platforms (Temu, Shein, AliExpress) that ship individual packages directly from China to US buyers

The volume of Section 321 entries has exploded. CBP processes roughly 4 million Section 321 shipments per day, up from about 770,000 per day in 2019.

The 2025-2026 Section 321 Changes

What Changed

Section 321 has been under increasing scrutiny. In 2025, the US government announced significant restrictions:

- Executive Order (April 2025): Eliminated Section 321 eligibility for most goods from China, Hong Kong, and Macau. Starting May 2, 2025, packages from these origins face either a 120% ad valorem duty or a flat $100 per-item fee (rising to $200 by June 2025).

- Congressional proposals: Multiple bills aim to lower the de minimis threshold or eliminate it entirely for countries without free trade agreements.

- Enhanced data requirements: CBP now requires more detailed data for Type 86 entries, including 10-digit HTS codes.

These changes primarily target the flood of low-value packages from China. For brands shipping from other countries, Section 321 still applies at the $800 threshold.

Impact on Ecommerce Brands

Brands sourcing from China need to rethink their logistics:

- Shipping directly from China to US consumers is no longer cost-effective for low-value items

- Bonded warehouses in North America become more attractive

- Canadian and Mexican fulfillment can still leverage Section 321 (for now)

- Duty drawback becomes more valuable as an alternative cost recovery mechanism

For European brands selling into the US, Section 321 remains fully functional for shipments under $800. This gives EU-based DTC brands a competitive advantage over China-based sellers.

What Is Duty Drawback?

The Basics

Duty drawback is a refund of customs duties, taxes, and fees paid on imported goods that are subsequently exported or destroyed. The program has existed since 1789 and is administered by CBP.

The logic is simple: if a brand imports materials or finished goods, pays duties, and then exports those goods (or goods made from those materials), the brand shouldn't be double-taxed. Duty drawback returns up to 99% of the duties paid.

Types of Duty Drawback

Three main types apply to ecommerce:

- Direct identification drawback: The exact imported goods are exported. For example, a brand imports 1,000 units from overseas, pays duties, then ships 200 of those units to Canadian customers. The brand can claim drawback on the duties paid for those 200 units.

- Substitution drawback: Commercially interchangeable goods are exported instead of the exact imported goods. For example, a brand imports cotton t-shirts from Vietnam and also makes cotton t-shirts domestically. If the domestic t-shirts are exported, the brand can claim drawback on the duties paid for the imported ones.

- Rejected merchandise drawback: This is the one most relevant to returns. If imported goods are returned by customers or rejected because they're defective, and those goods are then exported back to the origin country (or destroyed under customs supervision), the brand can recover the duties paid on those specific items.

With the integration to Business Central, resolving a claim in Claimlane automatically triggers all the necessary processes in our ERP. This means the customer service agent's work is complete the moment the claim is resolved in Claimlane.

Kasper Andersen, IT Director — Konges Sløjd

How Much Can Brands Recover?

The recovery depends on the duty rate and the volume of eligible exports or returns:

- Manufacturing drawback: Up to 99% of duties paid

- Unused merchandise drawback: Up to 99% of duties paid

- Rejected merchandise drawback: Up to 99% of duties paid

For a brand paying $500,000/year in import duties with a 25% export-or-return ratio, that's $125,000 in duties eligible for drawback. At a 99% recovery rate, the brand gets back approximately $123,750.

How Duty Drawback Connects to Returns

Returns as a Drawback Trigger

When a customer returns an imported product and that product is subsequently exported (sent back to the foreign supplier or shipped to an international customer), the brand may be eligible for rejected merchandise drawback.

The process works like this:

- Brand imports 500 units from Germany and pays $10,000 in duties

- 50 units are returned by US customers as defective

- Those 50 defective units are shipped back to the German supplier for replacement

- Brand files a drawback claim for the duties paid on those 50 units ($1,000)

- CBP processes the claim and refunds approximately $990

For brands with high return rates on imported products, this can recover significant amounts. A brand with a 20% return rate on imported goods could potentially recover drawback on all of those returned items, provided they're exported or destroyed.

Why Most Brands Don't Claim Drawback

Despite the savings, most ecommerce brands don't file for duty drawback. The reasons:

- Complexity: The filing process requires detailed import records (entry numbers, HTS codes, duties paid) matched against export records. This is paperwork-intensive.

- Time limits: Claims must be filed within 5 years of import and 3 years of export.

- Minimum thresholds: The administrative overhead only makes sense above a certain duty volume (typically $50,000+/year in duties paid).

- Lack of awareness: Many ecommerce brands simply don't know duty drawback exists.

Brands using a returns management platform that tracks return origins, destinations, and product data are better positioned to file drawback claims because the data is already captured.

Section 321 for Returns

Returning Products Under De Minimis

Section 321 isn't just for inbound shipments. It can also apply when returned products are shipped back into the US after being exported for repair or replacement.

Scenario: A US brand ships a defective product to a European repair facility. After repair, the product is shipped back to the US. If the repaired item's value is under $800, it can re-enter under Section 321 without additional duties.

This is particularly useful for brands handling international warranty claims where products need to be sent overseas for specialized repair and then returned to the customer.

Combining Section 321 and Duty Drawback

Brands can use both programs strategically:

- Inbound: Use Section 321 for individual DTC shipments under $800 to avoid duties on initial import

- Returns: When returned items are exported back to the supplier, file for duty drawback on any duties that were paid (on formal entries above $800)

- Re-imports: When repaired items come back from overseas, use Section 321 if under $800

The combination requires good record-keeping. Every shipment, return, and re-import needs documentation that ties back to the original import entry. Platforms like Claimlane that track claims from initiation through resolution with full product data (integrations with ecommerce platforms, shipping providers, and supplier systems) make this documentation much easier to maintain.

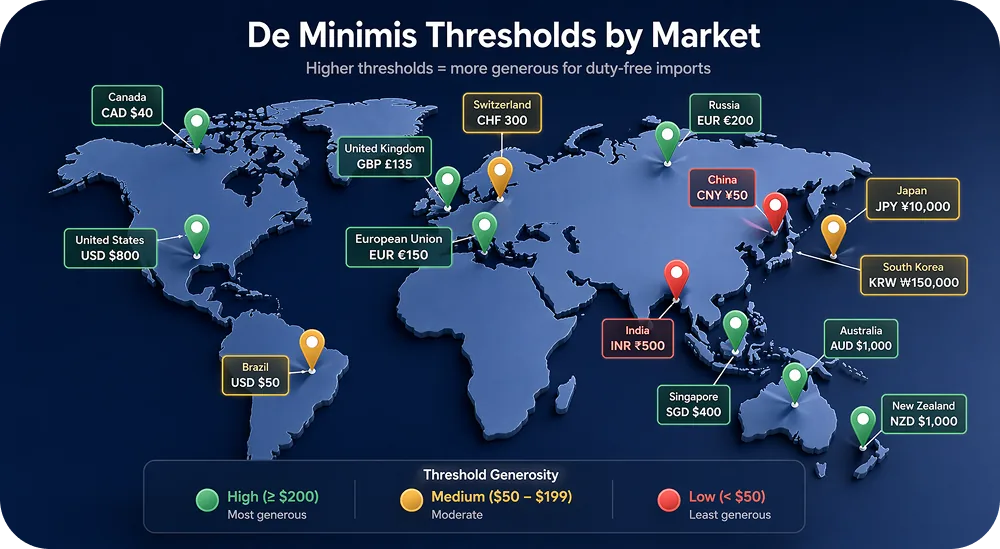

De Minimis Thresholds Around the World

The $800 US threshold is unusually high. Other countries have much lower limits:

| Country / Region | De Minimis Threshold | Notes |

|---|---|---|

| United States | $800 USD | Eliminated for CN/HK/Macau (2025) |

| Canada | $150 CAD | Raised from $20 in 2024 |

| European Union | €150 | VAT applies on all imports since 2021 |

| United Kingdom | £135 | VAT collected at point of sale |

| Australia | $1,000 AUD | GST on all goods regardless |

| Japan | ¥10,000 | Low threshold |

| China | ¥50 RMB | Effectively no de minimis |

For brands selling into multiple markets, understanding these thresholds determines whether it makes sense to ship direct-to-consumer from a central warehouse or to pre-position inventory in local fulfillment centers.

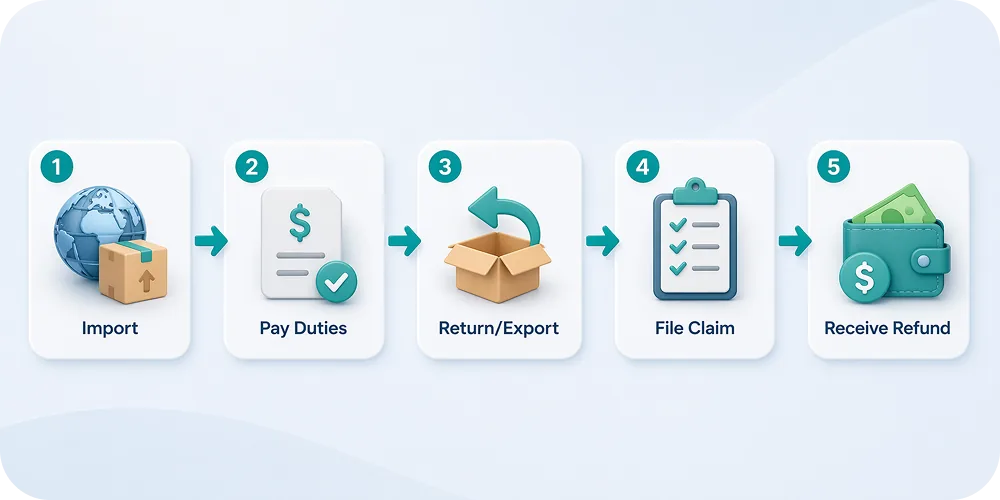

How to File for Duty Drawback

Step-by-Step Process

- Gather import documentation. Collect all entry summaries (CF 7501), commercial invoices, and proof of duties paid for the relevant import period.

- Match imports to exports/returns. Identify which imported goods were subsequently exported, destroyed, or returned and exported. This is where good returns data is critical.

- File the drawback claim. Submit electronically through CBP's ACE (Automated Commercial Environment) system. Include:

- Import entry numbers and dates

- Export documentation (bills of lading, export declarations)

- Proof of destruction (if applicable)

- Calculation of drawback amount

- CBP review. CBP reviews the claim, which can take 2 to 6 months. Accelerated payment is available for importers who post a bond.

- Receive refund. If approved, CBP issues a refund for up to 99% of the eligible duties.

Tools and Partners

Most brands don't handle drawback filing in-house. Options include:

- Customs brokers with drawback expertise: They manage the filing process for a percentage of the recovered amount (typically 10% to 25%)

- Drawback specialists: Companies like Comstock & Theakston, Alliance Trade Group, or Dutycalc that focus exclusively on duty drawback

- Trade management software: Platforms that automate the matching of imports to exports/returns

The key requirement is clean data. Every import needs a linked export or destruction record. Brands running their returns through a platform like Claimlane have an advantage because the analytics and claim data provide the product-level detail needed for drawback filings.

Practical Strategies for Ecommerce Brands

Small Brands (Under $100K in Annual Duties)

For brands paying less than $100,000/year in import duties:

- Focus on Section 321. If the average order value is under $800 and the brand can ship direct-to-consumer from an overseas location, Section 321 alone can eliminate most duty costs.

- Skip formal drawback filing. The administrative cost likely exceeds the recovery amount.

- Negotiate DDP terms with suppliers. Having the supplier handle duties (Delivered Duty Paid) simplifies the brand's customs burden.

Mid-Size Brands ($100K to $1M in Annual Duties)

For brands in this range:

- Use Section 321 strategically. Split fulfillment between a US warehouse (for domestic orders) and an international location (for Section 321 eligible orders).

- Start a drawback program. Engage a customs broker or drawback specialist. With $100K+ in duties and a 15% to 30% return/export rate, the recovery is meaningful.

- Track returns meticulously. Ensure the returns workflow captures all data needed for drawback claims: product SKU, original import entry, return date, and disposition (exported, destroyed, or restocked).

Large Brands ($1M+ in Annual Duties)

For brands at this scale:

- Dedicated trade compliance team or partner. Drawback at this volume requires systematic processes.

- Substitution drawback. Look for opportunities where domestically produced goods are exported, allowing drawback claims on duties paid for similar imported goods.

- Foreign trade zones (FTZs). Consider storing inventory in an FTZ to defer or eliminate duties on goods that are re-exported.

- Automate the link between returns and trade data. Use integrations that connect the returns platform, ERP, and customs broker systems.

- Focus on Section 321

- Skip formal drawback

- Negotiate DDP terms

- Strategic Section 321

- Start drawback program

- Track returns meticulously

- Dedicated compliance

- Substitution drawback

- Foreign trade zones

Common Mistakes to Avoid

With Section 321

- Splitting shipments artificially. CBP watches for brands splitting a single large order into multiple sub-$800 packages to game the threshold. This is called "structuring" and can result in penalties.

- Ignoring origin restrictions. Since the 2025 changes, goods from China, Hong Kong, and Macau no longer qualify. Brands must verify the origin country of every product.

- Not tracking 321 volumes. CBP requires certain data for Type 86 entries. Brands that don't provide it risk shipment holds and delays.

With Duty Drawback

- Missing the filing deadline. Claims must be filed within 5 years of import. Brands that wait too long lose the opportunity permanently.

- Poor record linkage. Every drawback claim requires a clear link between the original import (entry number, duty amount) and the subsequent export or destruction. Incomplete records = denied claims.

- Not claiming on returns. Many brands don't realize that returned and re-exported goods qualify for drawback. If a product is imported, returned by a customer, and then shipped back to the foreign supplier, that's a valid drawback claim.

The Role of Returns Data in Cross-Border Cost Recovery

Why Returns Platforms Matter

The missing link in most duty drawback programs is returns data. A customs broker can match import entries to export records, but they need to know which returned items were subsequently exported. That information lives in the returns management system.

Brands using Claimlane can pull detailed data on every return: what was returned, why, when the return was initiated, when it was received, and critically, what happened to the item after return (restocked, sent to supplier, destroyed). Rated 4.8/5 on G2 (read reviews), Claimlane captures the exact data trail that drawback filings require.

The forward-to-supplier feature is particularly relevant. When a defective product is returned and forwarded to the overseas supplier for replacement or credit, that's an export event that may trigger drawback eligibility.

Claimlane helps us capture every customer issue, resolve it for the customer, and feed that back to the supply chain to drive continuous improvement.

Henry Currer, Head of Operations — Swoon Furniture

.webp)