.webp)

What Is a Payment Reversal?

A payment reversal is any transaction that returns funds from a merchant back to a customer. It's an umbrella term that covers three distinct processes: authorization reversals, refunds, and chargebacks.

For ecommerce brands, payment reversals are a daily reality. Every return, every dispute, and every cancelled order involves some form of payment reversal. The type of reversal matters because each one has different costs, timelines, and impacts on the business.

Understanding how payment reversals work, and which type applies in each situation, helps brands minimise fees, reduce disputes and chargebacks, and keep their payment processing accounts in good standing.

The Three Types of Payment Reversals

Not all payment reversals are the same. The differences come down to timing, who initiates the reversal, and what it costs the merchant.

1. Authorization reversal

An authorization reversal happens before the transaction is fully settled. When a customer places an order, the payment processor puts a hold (authorization) on the funds. If the order is cancelled before the payment settles (typically within 24 to 48 hours), the merchant can release the hold through an authorization reversal.

Cost to merchant: Zero. No funds were actually transferred, so there are no processing fees to reverse.

When it happens: Order cancellations before shipment, duplicate transactions caught early, fraud flags during order review.

Timeline: The hold is released within 1 to 3 business days. The customer sees the pending charge disappear from their statement.

2. Refund

A refund is a new transaction where the merchant sends money back to the customer after the original payment has settled. Unlike an authorization reversal, the original transaction completed, and the refund is a separate transaction going in the opposite direction.

Cost to merchant: The merchant typically loses the original transaction fee (the payment processor doesn't refund its processing fee on the original charge). Some processors charge an additional refund processing fee.

When it happens: Product returns, order cancellations after shipment, price adjustments, customer service resolutions.

Timeline: 5 to 10 business days for the refund to appear on the customer's statement, depending on the payment method and bank.

3. Chargeback

What is a chargeback? A chargeback is a forced payment reversal initiated by the customer's bank, not the merchant. The customer contacts their bank to dispute a credit card charge, and the bank reverses the transaction without the merchant's consent. The merchant can contest the chargeback by submitting evidence, but the funds are pulled first and only returned if the dispute is won.

Sometimes called a credit card chargeback, transaction dispute, or return item chargeback in accounting contexts, the chargeback is the most expensive type of payment reversal a merchant can face.

Cost to merchant: The refunded amount plus a chargeback fee ($20 to $100 per incident). If the merchant loses the dispute, the money and the fee are gone. High chargeback ratios (above 1% of transactions) can trigger penalties from payment processors, including higher fees or account termination.

When it happens: Unauthorized transactions (stolen cards), products not received, products not as described, customer disputes, and friendly fraud (customer received the product but disputes the charge anyway).

Timeline: The customer can file a chargeback up to 120 days after the transaction (varies by card network). The dispute process takes 30 to 90 days.

How Chargebacks Work

A chargeback follows a specific process from filing to resolution:

- Customer files dispute. The customer contacts their bank or card issuer to dispute a charge, citing one of the standard reason codes (unauthorized transaction, product not received, product not as described, etc.).

- Bank reverses the charge. The customer's bank pulls the disputed amount from the merchant's account, plus a chargeback fee. This happens before any investigation.

- Merchant is notified. The merchant's payment processor sends a chargeback notification, including the reason code, the disputed amount, and a deadline for responding.

- Merchant submits evidence. Within the response window (typically 20-45 days), the merchant compiles evidence showing the transaction was legitimate.

- Bank reviews and decides. The customer's bank reviews the evidence and either reverses the chargeback (merchant wins) or upholds it (customer wins).

- Arbitration if disputed. If either party disagrees, the case can go to arbitration with Visa or Mastercard, but this is rare due to high fees.

The whole process takes 30-90 days. The merchant only gets the funds back if they win the dispute.

Payment Reversal vs. Refund vs. Chargeback: A Side-by-Side Comparison

The hierarchy of preference for merchants is clear: authorization reversals are free, refunds cost a transaction fee, and chargebacks cost a fee plus damage to the merchant's reputation with payment processors.

How is a chargeback filed?

Customers file a chargeback by contacting their bank or credit card issuer, not by contacting the merchant. They typically have 60-120 days from the transaction to file, depending on the card network. The customer provides their reason for disputing the charge, and the bank initiates the chargeback process on their behalf.

For merchants, this is significant because the merchant is often the last to know. By the time the chargeback notification arrives, the customer has already been refunded the disputed amount.

The fastest way to prevent chargebacks is to make refunds easier than chargebacks. If the customer can get a refund through a self-service portal in minutes, they have no reason to call their bank.

Why Chargebacks Are the Biggest Threat

Chargebacks deserve special attention because they're the most expensive and least controllable type of payment reversal.

The financial impact

Every chargeback costs the merchant:

- The full transaction amount (returned to the customer)

- A chargeback fee ($20 to $100)

- The cost of the product (if already shipped and not returned)

- Staff time to manage the dispute process

For a $75 order with a $25 chargeback fee, the total loss is $100 plus the cost of goods and labor. Multiply that across dozens or hundreds of chargebacks per month, and it becomes a significant line item.

What are chargeback fees?

A chargeback fee is a non-refundable fee charged by the payment processor when a chargeback is filed against the merchant, regardless of whether the merchant wins or loses the dispute. Fees range from $20 to $100 per chargeback depending on the processor and the merchant's risk tier.

Even if the merchant wins the dispute and the chargeback is reversed, the chargeback fee usually isn't refunded. This is one of the reasons chargebacks are so expensive: the merchant pays for the dispute process even when the customer's claim was unfounded.

The account health impact

Visa and Mastercard monitor chargeback ratios. If a merchant's chargeback rate exceeds 1% of transactions (Visa) or 1.5% (Mastercard), the merchant enters a monitoring program with escalating retail chargeback penalties:

- Warning: Merchant is notified and must submit a remediation plan.

- Fines: Monthly fines ranging from $5,000 to $25,000.

- Higher processing fees: The payment processor adds surcharges.

- Account termination: The processor closes the merchant's account. The merchant may be placed on the MATCH list (Member Alert to Control High-Risk Merchants), making it difficult to open a new processing account.

Friendly fraud: the hidden driver

Friendly fraud (also called first-party fraud) accounts for an estimated 60% to 80% of all chargebacks. This is when a customer makes a legitimate purchase, receives the product, and then disputes the charge with their bank.

Common reasons for friendly fraud:

- The customer forgot about the purchase

- Someone else in the household made the purchase

- The customer didn't recognize the merchant's billing descriptor

- The customer wanted a refund but didn't want to go through the return process

- The customer intentionally kept the product and disputed the charge

Friendly fraud is notoriously hard to prevent because the customer appears legitimate at every stage of the transaction.

Common Reasons for Payment Reversals in Ecommerce

Understanding why reversals happen is the first step toward reducing them.

Product returns

The most common and most legitimate reason. The customer received the product, wasn't satisfied, and requested a return and refund. This is a standard refund, fully within the merchant's control.

Brands that make the return process easy and fast have fewer chargebacks because customers get their money back through the proper channel instead of disputing the charge. A well-structured returns process is the first line of defence against unnecessary chargebacks.

Product not received

The customer claims the package never arrived. This can be a legitimate complaint (carrier lost the package, delivered to the wrong address) or friendly fraud (the customer received it but says they didn't).

Protection: Use carriers with delivery confirmation and signature requirements for high-value orders. Proactive tracking notifications reduce "not received" claims by keeping the customer informed throughout the delivery process. For guidance on handling these situations, see this guide on notifying customers during returns.

Product not as described

The customer says the product doesn't match what was shown on the website. This often happens with inaccurate product photos, missing size information, or vague product descriptions.

Protection: Invest in accurate product photography, detailed descriptions, size guides, and customer reviews. The better the product page, the fewer "not as described" disputes.

Unauthorized transactions

Someone used a stolen credit card to make a purchase. The legitimate cardholder discovers the charge and disputes it. This is true fraud, not friendly fraud.

Protection: Use fraud detection tools (Stripe Radar, Signifyd, Riskified) that analyze transaction signals like device fingerprint, IP geolocation, purchase history, and velocity checks.

Subscription billing issues

Customers forget they signed up for a subscription, can't figure out how to cancel, or didn't realize a free trial would convert to a paid subscription. These generate a disproportionate number of chargebacks.

Protection: Send reminder emails before subscription renewals, make the cancellation process obvious, and use clear billing descriptors.

How to Prevent Chargebacks

Prevention is significantly cheaper than fighting disputes. Here are the most effective strategies.

Make refunds easier than chargebacks

Customers file chargebacks when they can't get a refund through the merchant. If the return process requires three emails, a phone call, and two weeks of waiting, the customer will call their bank instead.

Self-service return portals, clear return policies, and fast refund processing all reduce chargebacks by making the legitimate path frictionless. Platforms like Claimlane automate the return and refund workflow so customers get resolution quickly without needing to contact support.

Use clear billing descriptors

The merchant name that appears on the customer's credit card statement should be recognizable. If the customer sees "TECH PAYMENTS LLC" instead of "[Brand Name]", they might not recognize the charge and dispute it.

Check the billing descriptor with the payment processor and make sure it includes the brand name. Some processors also support dynamic descriptors that include the product name or order number.

Send proactive communications

Order confirmation, shipping notification, delivery confirmation, and follow-up emails all reduce disputes. Each touchpoint reminds the customer what they bought, when it shipped, and when it arrived.

Implement fraud detection

Use the fraud detection tools built into payment processors (Stripe Radar, PayPal Seller Protection) or third-party tools (Signifyd, Riskified, ClearSale). These provide merchant chargeback protection by analysing transactions in real time and flagging high-risk orders for manual review. Some platforms also offer chargeback protection guarantees, where they reimburse the merchant for any chargebacks on transactions they approved.

Track delivery with proof

For orders above a certain threshold (many brands use $75 to $100), require delivery confirmation or signature. This provides evidence for "product not received" disputes.

Respond to chargebacks promptly

When a chargeback is filed, the merchant has a limited window (typically 20 to 45 days depending on the card network) to submit evidence disputing the claim. Responding with strong evidence (delivery confirmation, customer communications, signed agreements) wins back 20% to 40% of disputes on average.

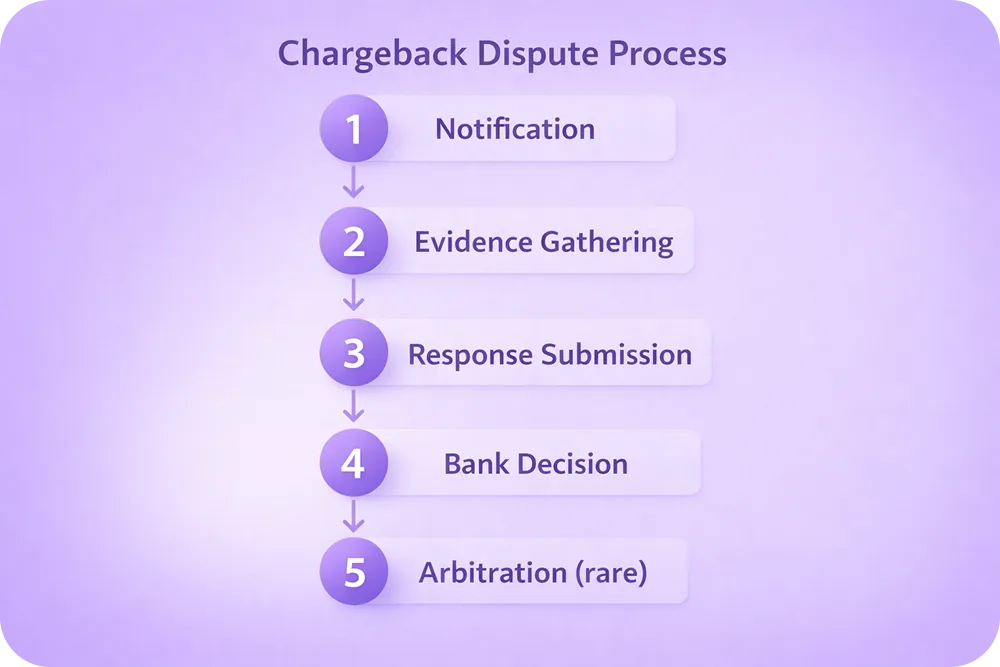

The Chargeback Dispute Process

Knowing how to respond to a chargeback within the deadline is the difference between recovering revenue and losing it. Here's how to fight chargebacks effectively, step by step from the merchant's perspective.

Step 1: Notification

The merchant receives a chargeback notification from their payment processor. The notification includes the reason code, the disputed amount, and the deadline for responding.

Step 2: Evidence gathering

The merchant collects evidence to contest the chargeback:

- Proof of delivery (tracking number, delivery confirmation, signature)

- Customer communications (emails, chat transcripts)

- Order details (what was ordered, when, shipping address)

- Return/refund policy that the customer agreed to

- Product description and photos matching what was delivered

- Previous transaction history with the customer

Step 3: Response submission

The merchant submits the evidence package (called a "representment") to their payment processor, who forwards it to the issuing bank.

Step 4: Bank decision

The customer's bank reviews the evidence and makes a decision. If the bank sides with the merchant, the chargeback is reversed, and the merchant keeps the funds (but typically still pays the chargeback fee). If the bank sides with the customer, the chargeback stands.

Step 5: Arbitration (rare)

If either party disagrees with the outcome, the case can go to arbitration with the card network (Visa or Mastercard). Arbitration fees are significant ($250 to $500), so this is rare and typically reserved for high-value disputes.

Payment Reversals and Returns: How They Connect

Returns and payment reversals are deeply connected. A smooth return process leads to merchant-initiated refunds (cheap and controlled). A broken return process leads to customer-initiated chargebacks (expensive and uncontrolled).

The math is simple:

- Processing a return and issuing a refund costs the merchant the product return shipping + processing labor + lost transaction fee. For a typical ecommerce order, that's $10 to $25.

- A chargeback on the same order costs the refund amount + chargeback fee + product loss + dispute management time. That's easily $50 to $150+.

Every chargeback prevented by a smooth return process is money saved. This is why brands investing in returns automation (through platforms like Claimlane and its self-service portal) see a measurable reduction in chargeback rates.

Chargeback Reversal: Can Merchants Get Chargebacks Overturned?

Average chargeback win rate when merchants submit evidence

Win rate on "product not received" disputes with delivery confirmation

Of all chargebacks are friendly fraud (not actual fraud)

A chargeback reversal happens when the merchant successfully disputes a chargeback and the bank reverses its original decision. Yes, merchants can win chargebacks, but the success rate varies.

Highest win rates

- Product received (customer claims not received): If the merchant has delivery confirmation with a matching address, win rates exceed 60%.

- Subscription cancellation: If the merchant can show the cancellation policy was communicated and the customer didn't cancel, win rates are strong.

Lowest win rates

- Unauthorized transaction (true fraud): If the card was genuinely stolen, the merchant rarely wins.

- Product not as described: Subjective disputes are hard to win because banks tend to side with cardholders.

Tips for winning disputes

- Respond within the deadline. Late responses are automatic losses.

- Submit all relevant evidence in one package. Banks typically review evidence once.

- Include tracking proof with delivery confirmation for "not received" disputes.

- Show the customer agreed to the return/refund policy at checkout.

- Include previous positive transaction history if the customer has bought from the brand before.

Monitoring and Managing Payment Reversals

Brands should track payment reversal data as closely as they track revenue and customer acquisition metrics.

Key metrics to monitor

- Chargeback ratio: Total chargebacks divided by total transactions. Keep this below 0.65% (Visa's early warning threshold) and well below 1%.

- Refund rate: Total refunds divided by total transactions. A rising refund rate may indicate product quality issues, inaccurate descriptions, or sizing problems.

- Dispute win rate: Percentage of contested chargebacks that the merchant wins. Track this to evaluate the effectiveness of the evidence submission process.

- Average days to refund: How long it takes from return request to refund processed. Longer timelines correlate with higher chargeback rates.

Actionable steps

- Set up alerts for chargeback ratio thresholds (0.5%, 0.75%, 1.0%).

- Audit high-chargeback products to identify if specific items generate disproportionate disputes.

- Review return reasons monthly to catch product or fulfillment issues early.

- Test billing descriptors by making a small purchase on a personal card to see how the brand name appears.

.webp)